This blog post explains how to calculate emissions according to the Carbon Border Adjustment Mechanism (CBAM) regulation. For a broader understanding of CBAM and its implications for businesses, we suggest reading our related article: Implications, Challenges, and Opportunities of the Carbon Border Adjustment Mechanism (CBAM).

CBAM requires companies to report actual emission data for imported goods, going beyond standard emission factors (EFs) to provide a more accurate picture of emissions. Depending on the imported goods, different emissions categories must be accounted for as stated in Annex I of the regulation. The total emissions should be reported in CO2 equivalent, often referred to as CO2e.

This approach poses new challenges for companies, as they must report verified data using established calculation methods. In this post, we provide an example of how to calculate the embedded emissions for a specific good under CBAM.

The regulation classifies goods as either simple or complex. A simple good is made from materials and fuels not covered by CBAM, meaning it has no embedded emissions. A complex good, on the other hand, is made using precursor goods that are included in CBAM. In this example, we calculate the emissions associated with a simple good.

In the case of complex goods, you can follow the same calculation steps with the difference that you need to add the emissions from the precursor goods used for its production to the total result. So, for complex goods, you can justify up to 20% of the total emissions using approved default EFs.

Since the regulation requires reporting both direct and indirect emissions from the production process, electricity consumption must be included in the calculation.

Note: All values in the calculation are used for this example and are not to be re-used in real reporting use cases!

In this example, we consider a company importing sintered iron ore from India into the EU. As an importer of a product CBAM covers, the company must report the emissions from this product’s production. We will outline the steps to calculate these embedded emissions in CO2e.

The classification and trade codes for goods covered by the regulation are listed in Annex I of the EU CBAM Implementing Regulation. Sintered iron ore is classified under the Combined Nomenclature (CN) with the following code:

This code is included in the scope of CBAM under iron and steel. For SAP users, the CN code of the goods should be documented in S4/HANA (Fiori -> Customs Management).

Relevant operations and flows involved in the production of the good, along with emissions sources, must be identified and included according to the regulation.

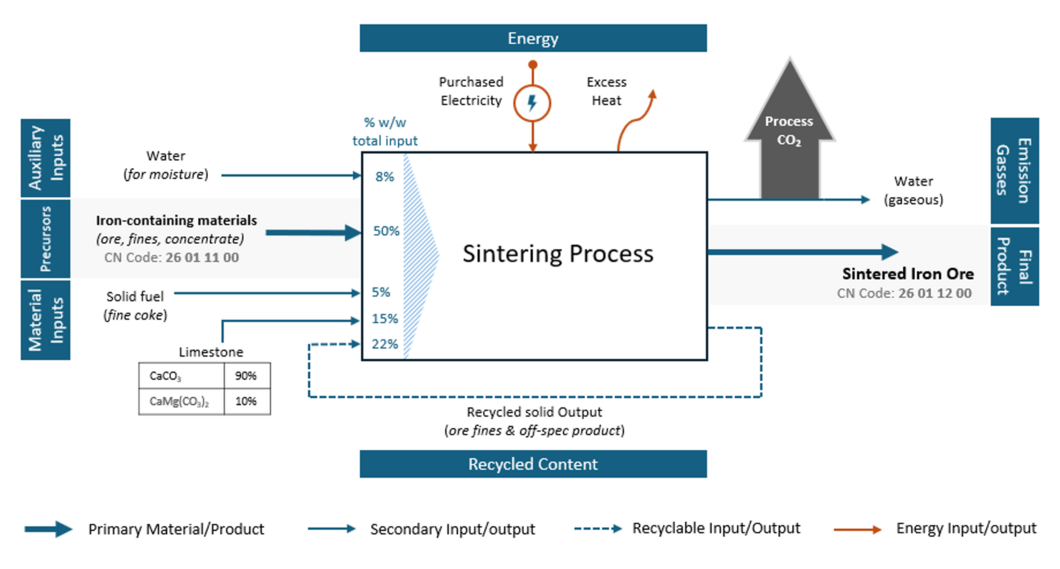

The sintering process of iron ore involves melting fine ore particles at high temperatures to form larger aggregates. During this process, fine iron ore particles are mixed with limestone and water to facilitate aggregation, while fine coke is added as a fuel source. Electricity is required to operate the equipment. The amount of each input depends on its quality, composition, and the technology used. Image 1 (below) provides a flow diagram to visualize this process. For this calculation example, a generic composition and proportion of inputs will be considered (% w/w presented in Image 1).

Image 1: Production process of sintered iron ore

The first task is to ensure that the targeted product is classified as a simple good under CBAM, which involves checking its precursors. In this case, the precursor is an iron-containing material, classified under the CN code 26 01 11 00. This code is not under the scope of CBAM. Thus, this process produces a simple CBAM good.

The next step is to identify which greenhouse gases should be included in the calculation for this product by reviewing Annex I of the regulation. For products classified under the CN code 26 01 12 00, only carbon dioxide needs to be considered.

Subsequently, review the CBAM Implementation Regulation, which outlines the flows to consider when calculating direct emissions for a particular “production route,” meaning alternative production processes. For this, it is important to check Table 1 in Annex II to identify the aggregated goods category under which the target product falls. Sintered iron ore is classified under the aggregated goods category as Sintered Ore, and Chapter 3 of the same Annex II offers guidance on key flows to analyze for this category. According to the regulation, the direct emissions calculation for sintered iron ore must include:

For simplicity, this example assumes that no precursors contain carbonates and that no flue gas cleaning is conducted as part of the production process. Therefore, the direct emissions calculation includes CO2 from burning the solid fuel (fine coke) and CO2 from the limestone calcination reaction.

Finally, it is necessary to review whether the process consumes electricity, as this is a source of indirect emissions for the regulation. Electricity is required to operate the equipment to produce sintered ore. Therefore, the carbon emissions associated with the production of the consumed electricity must also be included and reported.

The regulation mandates importers report emissions based on primary data from monitoring at the supplier’s production sites. Secondary data from reliable sources can only be used in specific, justified cases (only up to 20% for complex goods calculations). As mentioned above, default emissions factors are sourced from internationally trusted secondary data to calculate the process emissions.

Based on step 2, we need to calculate the direct emissions generated from two chemical reactions:

a. Limestone calcination

b. Coke burning

The chemical reaction of the burning of the different limestone components is as follows:

Based on Image 1, the quantity of limestone used for the production of 1 ton sintered ore is: 1.000 kg x 0.15(0.5+0.22+0.15) = 172.5 kg.

For this example, the composition of the limestone is 90% CaCO3 and 10% CaMg(CO3)2, therefore:

Thus, the calcination of 1 kg of limestone leads to:

= 420 gCO2 = 0.42 kg CO2

For the total emissions from limestone, we obtain:

For the coke emissions during burning, we use the default factor provided in Annex VIII, which states that the emission factor for coke, oven coke, and lignite coke is 0.107 kgCO2/MJ and that the net calorific value of this fuel is 28.2 MJ/kg.

Based on the data given in Image 1, in this example, the quantity of coke burned for obtaining 1 ton of sintered ore is:

=1.000 kg x0.05(0.5+0.22+0.15) = 57.5 kg

Then, we can obtain the total emissions from coke:

Burned Coke Quantity (kg) x Emissions of CO2e/kg Coke

= 57.5 kgCoke x 0.107 kgCO2/MJ x 28.2 MJ/kgCoke

= 173.5 kg CO2

Indirect emissions

The indirect emissions are related to the production of the consumed electricity. As the plant is located in India, it is necessary to use a local emission factor. According to the IEA1, the emission factor for electricity in India today is 0.853 CO2e/kWh.

For the plant energy consumption, we will consider the values reported for an average plant of sintering ore manufacturing2: 1.8 kWh/kg production.

Now we calculate the total emissions from electricity consumption:

Electricity Consumed Quantity (kWh) x emissions of CO2e / kWh local Electricity

= 1800 kWh x 0.853 kg CO2e/kWh

= 1535.4 kg CO2e

Total emissions

For total emissions, we sum the direct and the indirect emissions:

Total CO2e emissions = (direct emissions from raw materials use) + (direct emissions from fuel consumption) + (indirect emissions from electricity consumption)

= 72.45 + 173.5 + 1535.4 = 1,781.35 kg CO2e ~-> 1.78 metric tons of CO2e.

Therefore, for this example, the total emissions (as CO2e) for producing one ton of sintered ore is 1.78 tons.

1 Source: IEA, 2023 (reference year 2021)

Under CBAM, from January 2026, EU importers must register with national authorities and purchase and surrender CBAM emission certificates to prove the payment according to the total reported emissions.

The carbon price will change weekly based on the average price of EU ETS allowances (€/ton of CO2e) observed during the previous week. However, importers can obtain a discount if they prove that there has already been a carbon price paid in the country of production. The quantity to be discounted will be proportional to the carbon value that has been paid abroad.

This step accounts for any carbon costs that have already been paid in the country of origin (in our example, in India) under a local carbon pricing mechanism or carbon tax. The idea is to ensure that there is no double taxation or undue burden on the importer under CBAM.

According to the Guidance Document on CBAM Implementation for importers of goods into the EU, complex goods are defined as “goods other than simple goods.” They are products that consist of multiple components and often undergo various stages of processing, and the mechanism primarily focuses on specific sectors and goods that are energy-intensive and have a high carbon footprint, such as cement.

For complex goods, the calculation steps are the same as for simple goods but must also include emissions from producing the precursors and indirect emissions from purchased electricity. An example of a complex good is iron ore pellets made from iron ore concentrates, additives, and other bonding chemicals.